American consumers paid over $130 billion in credit card interest and fees in 2022, with balance transfer fees averaging 3% to 5% of the transferred amount while ongoing interest rates often exceed 20% APR. This makes the choice between upfront fees and accruing interest a critical financial decision for debt management (Consumer Financial Protection Bureau). For instance, transferring a $10,000 balance might incur a $300–$500 fee immediately, versus $2,000+ in interest over a year at 20% APR without payoff (NerdWallet).

Understanding Balance Transfer Fees

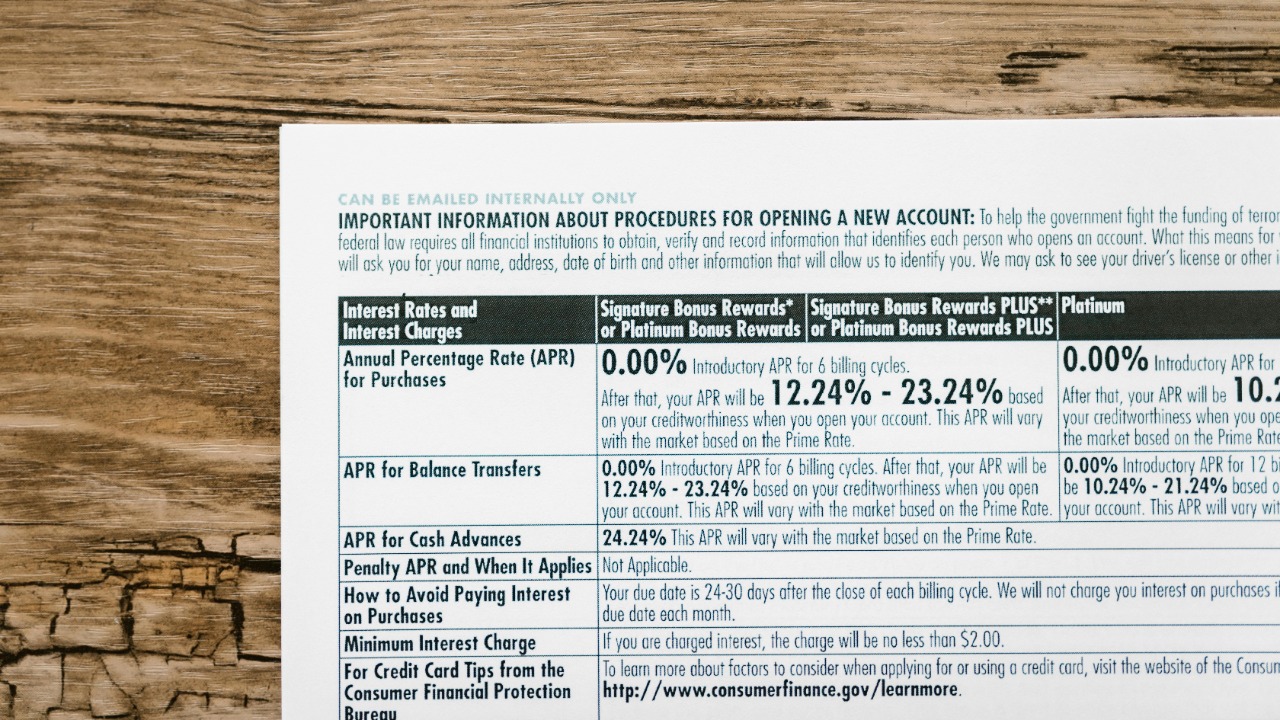

Balance transfer fees are charged as a percentage of the transferred amount, typically ranging from 3% to 5%, with some cards capping it at $50 per transfer. For example, the Chase Slate Edge card charges 3% on transfers within the first 60 days (Chase). These fees are non-refundable and added to the new card’s balance, potentially increasing the total debt if not paid off quickly (Bankrate).

In 2023, the average balance transfer fee rose to 4.2% due to market adjustments, affecting millions of users seeking lower introductory APRs (Forbes). This increase reflects broader economic trends and the demand for credit relief options, making it crucial for consumers to weigh the cost of these fees against potential savings from lower interest rates.

In addition to the direct costs, balance transfer fees can also impact your credit score indirectly. When you transfer a balance, the new card’s credit limit utilization ratio may increase if the balance is significant compared to the card’s limit. This can temporarily lower your credit score, affecting your ability to secure favorable terms on future credit products. Additionally, some cards may offer promotional periods with no balance transfer fees, but these offers are typically reserved for applicants with excellent credit scores, further emphasizing the importance of maintaining a strong credit profile (Experian).

The Mechanics of Credit Card Interest

Credit card interest is calculated daily based on the annual percentage rate (APR), which averaged 20.75% for new credit card offers as of Q2 2024, compounding on unpaid balances (Federal Reserve). For a $5,000 balance carried at 21% APR over 12 months with minimum payments, interest could total approximately $1,050, far exceeding typical transfer fees if the balance isn’t cleared during a 0% intro period (Credit Karma).

Variable APRs can fluctuate with the prime rate; the Federal Reserve’s rate hikes in 2022–2023 pushed average card APRs up by 5 percentage points (CNBC). This volatility underscores the importance of understanding how interest accrues and the potential financial impact of carrying a balance without a strategic payoff plan.

Understanding the compounding nature of credit card interest is crucial for effective debt management. Interest compounds daily, meaning that each day’s interest is calculated on the previous day’s balance, including any accrued interest. This compounding effect can significantly increase the total cost of carrying a balance over time. For instance, if you only make minimum payments, which often cover just the interest and a small portion of the principal, the balance can take years to pay off, costing thousands more in interest than the original debt amount (Investopedia).

Comparing Costs: Fees vs. Interest Scenarios

For a $3,000 transfer on a card with a 3% fee ($90 cost) and 18-month 0% intro APR, the fee is the only cost if paid off in time, versus $540 in interest on the original card at 18% APR over the same period (The Balance). This scenario highlights the potential savings of using balance transfers strategically to minimize interest payments.

If payoff extends beyond the intro period to a 22% ongoing APR, post-intro interest on the remaining balance could add $200+ monthly, making the initial fee seem minor in hindsight (Investopedia). A Consumer Reports survey in 2023 found 40% of balance transfer users underestimated post-intro interest, leading to net costs 2–3 times higher than the fee alone (Consumer Reports).

Another critical factor in comparing costs is the impact of introductory APR periods on long-term financial health. While a 0% intro APR can provide temporary relief, it is essential to have a clear payoff plan before the standard rate kicks in. Consumers often underestimate the challenge of paying off large balances within the promotional period, leading to unexpected financial strain when the regular APR applies. Additionally, some cards may revert to a penalty APR if a payment is missed during the intro period, further complicating the cost-benefit analysis of balance transfers (CreditCards.com).

Strategies to Minimize Total Costs

Opt for cards with 0% intro APR periods of 15–21 months, like the Citi Simplicity card offering 21 months on transfers, to amortize the fee over time without interest accrual (Citi). Calculating break-even points using tools from sites like Bankrate can help determine the most cost-effective strategy; for instance, for a 4% fee on $8,000, the intro period must exceed 8 months at 19% original APR to save money (Bankrate).

Avoid multiple transfers to prevent stacking fees; FDIC data shows serial transfers increased average household credit card debt by 15% in 2022 (FDIC). By carefully selecting balance transfer offers and managing payoff timelines, consumers can effectively reduce their overall debt burden and avoid unnecessary financial strain.

To further minimize costs, consumers should consider consolidating multiple high-interest debts into a single balance transfer. This strategy can simplify payments and reduce the overall interest burden if managed correctly. However, it’s crucial to avoid the temptation to accumulate new debt on the original cards once the balances are transferred. Maintaining discipline in spending and focusing on debt reduction can prevent the cycle of debt from continuing. Additionally, setting up automatic payments can ensure timely payments, avoiding late fees and potential increases in interest rates (Consumer Financial Protection Bureau).

More From TheDailyOverview

- Dave Ramsey warns to stop 401(k) contributions

- 11 night jobs you can do from home (not exciting but steady)

- Small U.S. cities ready to boom next

- 19 things boomers should never sell no matter what

Cole Whitaker focuses on the fundamentals of money management, helping readers make smarter decisions around income, spending, saving, and long-term financial stability. His writing emphasizes clarity, discipline, and practical systems that work in real life. At The Daily Overview, Cole breaks down personal finance topics into straightforward guidance readers can apply immediately.