As men reach their 40s, financial stability becomes more important than ever. While some may already have a solid foundation, fine-tuning budgeting habits can ensure a secure future. Here are nine essential practices that can help manage finances effectively during this crucial decade.

1. Prioritize Emergency Savings

Establishing a robust emergency fund is vital for financial security. In your 40s, unexpected expenses, such as medical emergencies or home repairs, can arise. Aim to save three to six months’ worth of living expenses to safeguard against unforeseen financial challenges. Consider using high-yield savings accounts from banks like Ally or Discover to grow your savings efficiently.

Regular contributions, no matter how small, can gradually build a substantial emergency fund. Automating transfers from your checking account to your savings account can facilitate consistent saving without the need for constant vigilance. This approach not only provides peace of mind but also prevents you from dipping into long-term savings when emergencies occur.

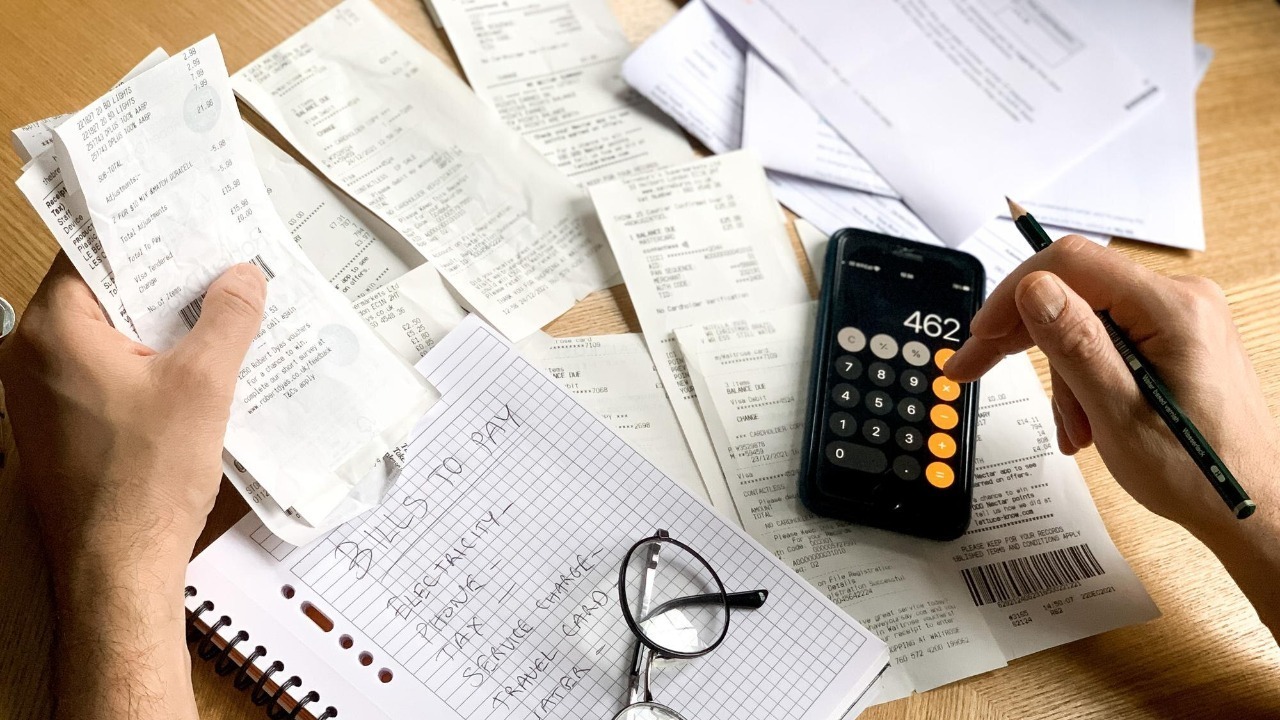

2. Track and Review Monthly Expenses

Monitoring monthly expenses helps identify spending patterns and areas for potential savings. Utilize budgeting apps like Mint or YNAB to categorize transactions and visualize spending habits. This insight can help you make informed decisions about where to cut back.

Make it a habit to review these expenses at the end of each month. Identifying trends early allows for adjustments before habits become problematic. This practice not only promotes financial discipline but also aids in aligning your spending with your long-term financial goals.

3. Automate Bill Payments

Late fees and interest charges can add unnecessary strain on your finances. Automating bill payments ensures that you never miss a due date, which can help maintain a good credit score. Set up automatic payments for recurring expenses such as utilities, mortgage, and credit card bills.

Most banks and service providers offer options to schedule payments automatically. By taking advantage of these services, you can avoid the stress of remembering each due date and instead focus on other financial priorities.

4. Diversify Investment Portfolios

Diversification is key to reducing risk in your investment portfolio. As you approach retirement age, it’s crucial to have a mix of asset classes, including stocks, bonds, and real estate, which can help balance potential gains and risks.

Consider consulting a financial advisor to tailor a diversification strategy that aligns with your risk tolerance and retirement goals. Resources like financial planning guides can provide further insights into making informed investment decisions.

5. Limit Discretionary Spending

While it’s important to enjoy the fruits of your labor, keeping discretionary spending in check ensures you don’t derail long-term financial goals. Dining out, impulse purchases, and luxury items can quickly add up.

Set a monthly limit for discretionary expenses and prioritize spending that aligns with your values and goals. This conscious approach allows for enjoyable experiences without compromising financial security.

6. Plan for Retirement

In your 40s, planning for retirement should be a top priority. Evaluate your retirement savings plan, such as a 401(k) or IRA, and adjust contributions to maximize potential growth. If your employer offers a matching contribution, ensure you’re contributing enough to take full advantage of this benefit.

It’s also advisable to periodically reassess your retirement goals and timelines. According to research, setting clear, achievable retirement goals can significantly impact your savings behavior and motivation.

7. Regularly Reassess Insurance Needs

Your insurance needs may evolve as you age. Regularly review your life, health, and property insurance policies to ensure they provide adequate coverage. Changes in family dynamics, health status, or asset value may necessitate policy adjustments.

Consult with an insurance advisor to explore options that fit your current situation. This proactive approach can prevent potential coverage gaps and ensure that your loved ones are financially protected.

8. Set and Stick to Financial Goals

Setting specific financial goals provides direction and motivation. Whether it’s saving for a child’s education, paying off a mortgage, or planning a dream vacation, having clear objectives helps focus financial efforts.

Break down larger goals into smaller, manageable milestones. This method not only makes the process less overwhelming but also allows for regular progress tracking. Achieving these milestones can boost confidence and reinforce positive financial habits.

9. Stay Informed on Financial Trends

Keeping abreast of financial trends can provide valuable insights into economic shifts and investment opportunities. Subscribing to financial news outlets or following finance experts on social media can help you stay informed.

Engaging with resources such as Yahoo Finance or academic articles can deepen your understanding of financial markets and strategies. This knowledge empowers you to make informed decisions that align with your financial goals.

Cole Whitaker focuses on the fundamentals of money management, helping readers make smarter decisions around income, spending, saving, and long-term financial stability. His writing emphasizes clarity, discipline, and practical systems that work in real life. At The Daily Overview, Cole breaks down personal finance topics into straightforward guidance readers can apply immediately.