The Federal Reserve recently cut interest rates, significantly impacting mortgage and loan costs across the United States. A $300,000 mortgage now has a different monthly cost, reflecting these changes. Additionally, the cost of an $80,000 home equity loan has also been affected.

Impact of the Federal Reserve’s Interest Rate Cut

The Federal Reserve’s decision to cut interest rates comes amid a broader economic strategy to stimulate growth and manage inflation. By lowering the cost of borrowing, the Fed aims to encourage spending and investment, which can help bolster economic activity. This decision has immediate effects on the housing market, as lower interest rates typically make mortgages more affordable, potentially increasing demand for homes.

For consumers, the rate cut means reduced costs for various loans, including mortgages and home equity loans. New borrowers can benefit from lower monthly payments, while existing homeowners might consider refinancing to take advantage of the lower rates. The specific rate changes have implications for both new and existing mortgages, making it crucial for homeowners and buyers to understand how these adjustments affect their financial planning.

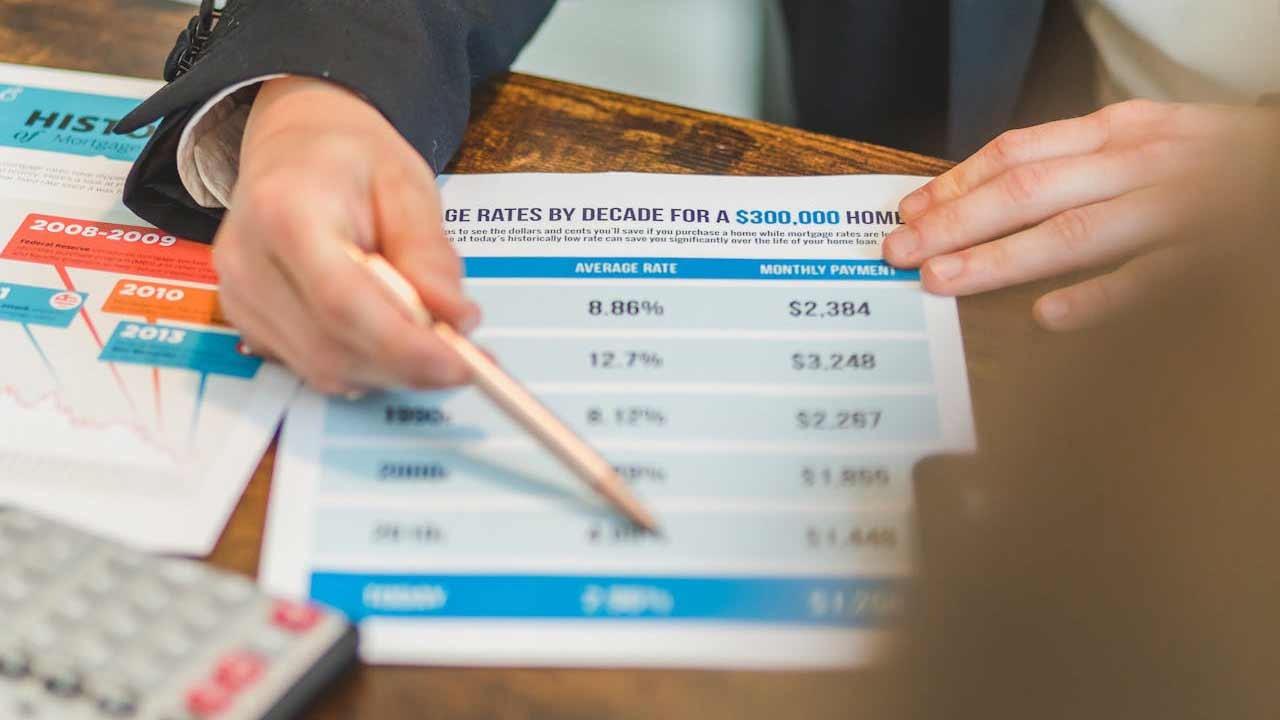

Monthly Cost of a $300,000 Mortgage

Following the Federal Reserve’s interest rate cut, the monthly payment for a $300,000 mortgage has decreased. According to CBS News, the new monthly cost reflects the lower interest rates, making homeownership more accessible for many potential buyers. This reduction in monthly payments can significantly impact household budgets, allowing for more disposable income or savings.

Comparing these new payments to those prior to the rate cut highlights the financial benefits for homebuyers. The decrease in monthly costs can make a substantial difference over the life of a mortgage, potentially saving homeowners thousands of dollars. For those considering purchasing a home, these changes present an opportunity to enter the market at a more affordable rate.

In addition to the immediate reduction in monthly payments, the lower interest rates can also affect the overall affordability of homes. Potential buyers might find that they qualify for larger loans than before, given the reduced interest burden. This can expand their options in the housing market, allowing them to consider properties that were previously out of reach. Moreover, the lower rates can also encourage existing homeowners to refinance their current mortgages, locking in the reduced rates for future savings. This strategic move can lead to substantial long-term financial benefits, as even a small reduction in interest rates can translate into significant savings over the life of a 30-year mortgage.

Changes in Home Equity Loan Costs

The interest rate cut has also altered the monthly cost of an $80,000 home equity loan. As reported by MSN, homeowners can now expect lower monthly payments, making it more attractive to tap into their home equity for renovations, debt consolidation, or other financial needs. This change can provide homeowners with more flexibility in managing their finances.

When comparing these new costs to those before the rate cut, the financial advantages become clear. Lower monthly payments can ease the burden on homeowners, allowing them to allocate funds to other priorities. For those considering a home equity loan, the current environment offers a favorable opportunity to secure financing at a reduced cost.

Furthermore, the reduced costs associated with home equity loans can stimulate economic activity by enabling homeowners to access funds for various purposes. For instance, homeowners might use the equity to invest in home improvements, which can increase the property’s value and enhance living conditions. Additionally, the lower rates can make it more feasible for homeowners to consolidate higher-interest debts, such as credit card balances, into a single, more manageable payment. This financial flexibility can improve household cash flow and reduce financial stress, making it easier for families to manage their budgets and plan for future expenses.

Long-Term Implications for Homeowners and Buyers

The long-term implications of the Federal Reserve’s interest rate cut on the housing market are significant. Sustained low rates could lead to increased borrowing and home purchasing, as more individuals find it financially feasible to buy homes. This trend could drive demand in the housing market, potentially leading to higher home prices over time.

Experts suggest that while low rates are beneficial for borrowers, they may also lead to increased competition among buyers, particularly in desirable areas. As the market adjusts to these changes, potential fluctuations in interest rates could impact future borrowing decisions. Homeowners and buyers should remain informed about economic trends and consider how potential rate changes might affect their financial strategies.

Over the long term, the sustained low interest rates could also influence the types of homes being built and purchased. Builders might respond to increased demand by constructing more homes, potentially leading to a more diverse range of housing options in the market. However, this increased activity could also strain resources and labor, potentially driving up construction costs. For buyers, the competitive market conditions might necessitate quicker decision-making and a more strategic approach to purchasing. Additionally, as more people enter the market, there could be a shift in demographics, with younger buyers taking advantage of the favorable conditions to secure their first homes. This demographic shift could have lasting impacts on community development and local economies.

Silas Redman writes about the structure of modern banking, financial regulations, and the rules that govern money movement. His work examines how institutions, policies, and compliance frameworks affect individuals and businesses alike. At The Daily Overview, Silas aims to help readers better understand the systems operating behind everyday financial decisions.