Reaching a savings goal of $50,000 might seem daunting, but with a strategic approach, it’s entirely achievable. By setting clear objectives and making informed financial decisions, you can steadily build your savings. Here are 11 straightforward steps to help you reach that $50K milestone.

Set Clear Financial Goals

Begin by defining what you want to achieve with your savings. Whether it’s buying a home, starting a business, or securing your retirement, having a clear goal will motivate you to stay on track. Consider using tools like the SMART criteria—Specific, Measurable, Achievable, Relevant, and Time-bound—to outline your objectives.

For example, if your goal is to save for a down payment on a house, determine the exact amount you need and the timeline for achieving it. This clarity will guide your financial decisions and help you prioritize your spending and saving habits.

Create a Realistic Budget

A budget is essential for managing your finances effectively. Start by listing your monthly income and expenses, including fixed costs like rent and utilities, as well as variable expenses such as groceries and entertainment. Use budgeting apps to track your spending and identify areas where you can cut back.

Ensure your budget is realistic and flexible enough to accommodate unexpected expenses. Regularly review and adjust it to reflect changes in your financial situation, ensuring you stay on course to meet your savings goal.

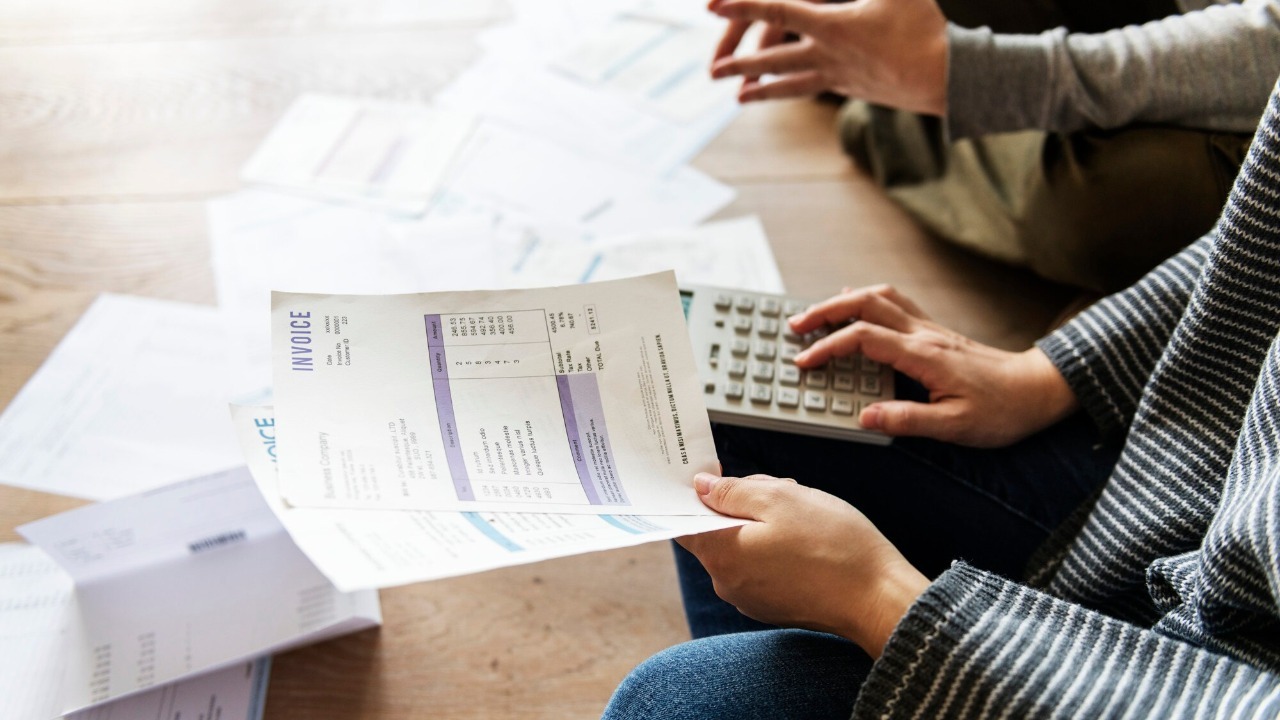

Track Your Expenses

Monitoring your spending is crucial for identifying unnecessary expenses. Keep a detailed record of every purchase, no matter how small. This practice will help you understand your spending habits and make informed decisions about where to cut back.

Consider using apps like Expensify or PocketGuard to automate this process. By regularly reviewing your expenses, you can identify patterns and make adjustments to ensure you’re saving as much as possible each month.

Cut Unnecessary Spending

Once you’ve tracked your expenses, identify areas where you can reduce spending. This might include dining out less frequently, canceling unused subscriptions, or opting for generic brands instead of name brands.

Small changes can add up over time, significantly boosting your savings. For instance, brewing coffee at home instead of buying it daily could save you hundreds of dollars annually. Prioritize needs over wants to maximize your savings potential.

Automate Your Savings

Automating your savings can help you stay consistent and disciplined. Set up automatic transfers from your checking account to your savings account each payday. This “pay yourself first” strategy ensures that saving becomes a priority rather than an afterthought.

Many banks offer tools to automate savings, such as rounding up purchases to the nearest dollar and transferring the difference to your savings account. This effortless approach can steadily increase your savings over time.

Increase Your Income

Boosting your income can accelerate your savings journey. Consider taking on a side hustle, such as freelancing, tutoring, or driving for a rideshare service. These additional income streams can supplement your primary earnings and help you reach your savings goal faster.

Additionally, explore opportunities for advancement in your current job, such as asking for a raise or seeking promotions. Increasing your income not only enhances your savings potential but also improves your overall financial security.

Build an Emergency Fund

An emergency fund is a financial safety net that can prevent you from dipping into your savings during unexpected situations. Aim to save three to six months’ worth of living expenses in a separate account dedicated to emergencies.

This fund will provide peace of mind and financial stability, allowing you to focus on reaching your $50K savings goal without interruptions. Prioritize building this fund before aggressively pursuing other financial objectives.

Pay Off High-Interest Debt

High-interest debt can significantly hinder your savings progress. Focus on paying off debts with the highest interest rates first, such as credit card balances. This strategy, known as the avalanche method, minimizes the amount of interest you pay over time.

Once high-interest debts are eliminated, you can redirect those payments toward your savings. This approach not only accelerates your savings growth but also improves your overall financial health.

Take Advantage of Employer Benefits

Many employers offer benefits that can enhance your savings efforts. For instance, if your employer offers a 401(k) match, contribute enough to take full advantage of this benefit. It’s essentially free money that can significantly boost your retirement savings.

Additionally, explore other benefits such as health savings accounts (HSAs) or flexible spending accounts (FSAs), which offer tax advantages and can help you save on healthcare expenses.

Invest Wisely

Investing can be a powerful tool for growing your savings. Consider diversifying your investments across different asset classes, such as stocks, bonds, and real estate, to balance risk and reward. Use platforms like Vanguard or Fidelity to manage your investments efficiently.

Educate yourself on investment strategies and seek professional advice if needed. Wise investing can help your savings grow faster than traditional savings accounts, bringing you closer to your $50K goal.

Review and Adjust Regularly

Regularly reviewing your financial plan is essential for staying on track. Set aside time each month to assess your progress, evaluate your budget, and make necessary adjustments. This proactive approach ensures that your financial strategy remains aligned with your goals.

Life circumstances can change, and your financial plan should adapt accordingly. By staying flexible and responsive, you can overcome challenges and continue progressing toward your $50K savings target.

Cole Whitaker focuses on the fundamentals of money management, helping readers make smarter decisions around income, spending, saving, and long-term financial stability. His writing emphasizes clarity, discipline, and practical systems that work in real life. At The Daily Overview, Cole breaks down personal finance topics into straightforward guidance readers can apply immediately.