In today’s fluctuating real estate market, many homeowners are overlooking a potentially profitable opportunity: refinancing their mortgages. With interest rates experiencing shifts and economic conditions evolving post-pandemic, understanding the right moment to refinance can lead to significant savings. Homeowners who stay informed about market trends and financial strategies can capitalize on these opportunities.

Understanding the Current Mortgage Climate

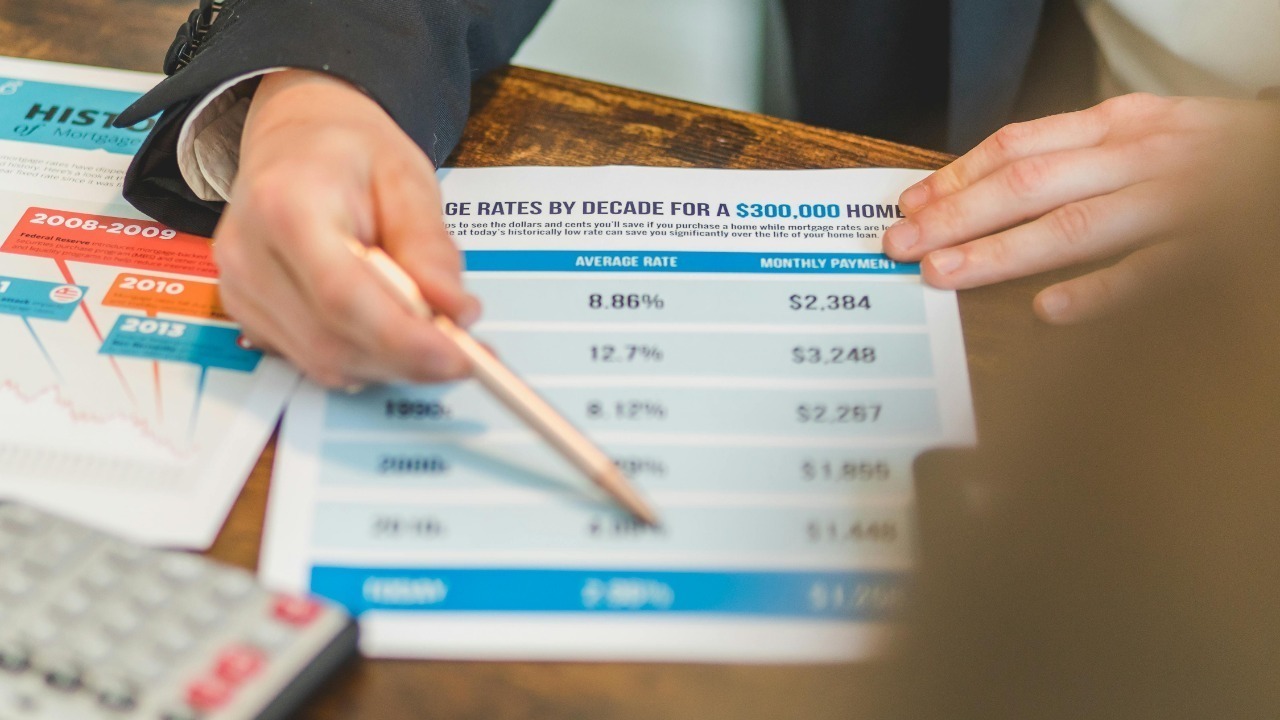

Recent trends in mortgage rates reveal a complex interplay between economic policies and market reactions. The Federal Reserve’s decisions significantly impact interest rates, as seen in their recent moves to adjust rates in response to inflation and employment data. Such adjustments ripple through the mortgage market, influencing the rates available to consumers. According to a recent report, even slight changes in the federal funds rate can lead to noticeable shifts in mortgage rates, altering the refinancing landscape.

Economic conditions such as inflation and employment levels also play a crucial role in shaping homeowner decisions. With inflation affecting purchasing power and job stability influencing financial confidence, these factors can either encourage or deter refinancing. As the economy continues to stabilize post-pandemic, homeowners must stay vigilant, considering not only current conditions but also market predictions. Analysts suggest that future rate adjustments could present more favorable refinancing opportunities, but timing remains key.

The Financial Benefits of Refinancing

Refinancing offers several financial benefits, chief among them the potential to reduce monthly payments. By securing a lower interest rate, homeowners can significantly lower their monthly mortgage expenses, freeing up cash flow for other household needs or investments. For example, a homeowner with a 30-year fixed-rate mortgage at 5% could refinance to a rate of 3.5%, saving hundreds of dollars each month.

Beyond the immediate reduction in monthly payments, refinancing can lead to substantial long-term savings. By calculating the total possible savings over the life of a refinanced loan, homeowners can see the true value of refinancing. For instance, switching from a 30-year mortgage to a 15-year one with a lower rate not only decreases interest payments but also helps in building equity faster. This accelerated equity accumulation can enhance a homeowner’s financial standing, providing more leverage in future financial endeavors.

Common Misconceptions and Missed Opportunities

Many homeowners are dissuaded from refinancing due to misconceptions about costs. There’s a prevalent belief that refinancing is prohibitively expensive, involving high upfront fees that negate any potential savings. However, many lenders offer competitive rates and fees, making the process more accessible than assumed. It’s crucial to shop around and compare different lenders to find the most beneficial terms.

Timing is another critical factor often misunderstood. Homeowners frequently miss optimal refinancing windows because they aren’t aware of the signs indicating a good time to refinance. Recognizing these moments requires a careful analysis of market trends and personal financial circumstances. Furthermore, a lack of financial literacy can deter homeowners from making informed decisions. Understanding how to evaluate refinancing options, such as adjusting loan terms or changing interest types, is essential for maximizing benefits.

Disparities in Refinancing Opportunities

Socioeconomic factors heavily influence access to refinancing opportunities. Income inequality can limit options for lower-income homeowners, who may face higher barriers to refinancing due to credit requirements or a lack of financial resources. This disparity is highlighted in a study by JPMorgan Chase, which examines the gap in refinancing trends during the COVID-19 pandemic.

Geographic disparities also play a role, as regional differences in housing markets and economic conditions affect refinancing trends. In some areas, high home values and strong market demand can create more favorable refinancing conditions. Conversely, in regions with stagnant property values or economic downturns, homeowners might face more challenges. Policy implications are significant, as changes in regulations could help equalize access to refinancing, offering more opportunities for diverse demographics.

Expert Tips for Timing Your Refinance

To effectively time a refinance, homeowners should monitor key economic indicators. Signs such as declining interest rates, reduced inflation, and stable employment figures can suggest a beneficial refinancing moment. Keeping an eye on these indicators helps homeowners anticipate favorable conditions, allowing them to act swiftly when opportunities arise.

Consulting professionals is another important step. Financial advisors and mortgage experts can provide personalized advice, helping homeowners navigate the complexities of refinancing. These experts offer insights into appropriate timing and strategies, ensuring that decisions align with long-term financial goals. Additionally, conducting a thorough personal financial assessment is crucial. Evaluating current mortgage terms, interest rates, and financial objectives can help determine if refinancing is the right move. By understanding personal circumstances and market conditions, homeowners can make informed refinancing decisions that enhance their financial well-being.

Elias Broderick specializes in residential and commercial real estate, with a focus on market cycles, property fundamentals, and investment strategy. His writing translates complex housing and development trends into clear insights for both new and experienced investors. At The Daily Overview, Elias explores how real estate fits into long-term wealth planning.