The Federal Reserve’s recent announcement of its first rate cut of 2025 marks a significant shift in monetary policy, offering potential relief for borrowers. This decision, covered in recent financial reporting, is seen as an opportunity for strategic financial actions, directly influencing personal loan rates by potentially lowering borrowing costs in the near term. As of late September 2025, experts are analyzing how this shift compares to prior steady-rate periods, urging consumers to act swiftly on emerging opportunities.

The Federal Reserve’s First Rate Cut of 2025

The Federal Reserve’s decision to implement its first rate cut of 2025 has broken from previous rate-holding policies, creating immediate market reactions. This move, as reported by CNBC, signals a departure from the Fed’s earlier stance of maintaining steady rates amid fluctuating economic indicators. The cut, which took place in early autumn 2025, is designed to stimulate economic activity by making borrowing cheaper, thereby encouraging spending and investment.

The mechanics of this federal funds rate adjustment are crucial to understanding its impact. As detailed by The Motley Fool, the rate cut influences the banking system by lowering the cost of borrowing for banks, which in turn affects consumer lending benchmarks. This transmission through the financial system is expected to lower interest rates on various loans, including personal loans, making it a pivotal moment for borrowers.

Comparisons to prior Federal Reserve decisions highlight what has changed in 2025 to prompt this rate cut. According to CNBC, evolving economic indicators, such as inflation rates and employment figures, have played a significant role in this decision. The Fed’s move reflects a response to these changes, aiming to support economic growth and stability.

In addition to stimulating borrowing, the rate cut is also expected to have a significant impact on the stock market. Historically, lower interest rates tend to boost stock prices as investors seek higher returns than those offered by bonds and savings accounts. This shift in investor behavior can lead to increased capital inflows into equities, potentially driving up market indices. Furthermore, businesses may find it cheaper to finance expansion projects, which can enhance corporate earnings and further support stock valuations.

Moreover, the rate cut reflects the Federal Reserve’s proactive approach to managing economic growth amid global uncertainties. As noted by CNBC, geopolitical tensions and international trade dynamics have added layers of complexity to economic forecasting. By adjusting rates, the Fed aims to cushion the U.S. economy against potential external shocks, ensuring a stable environment for both consumers and businesses.

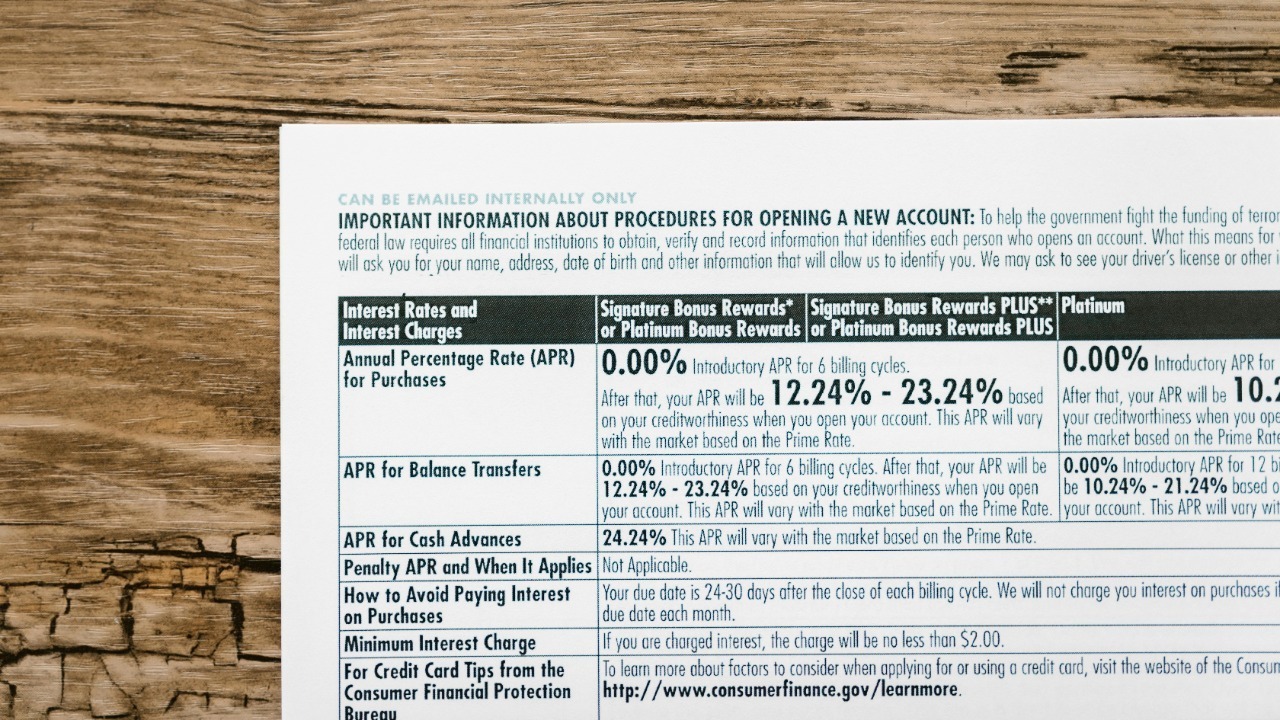

Direct Impacts on Personal Loan Rates

The first rate cut of 2025 is expected to lower average personal loan APRs, with lenders adjusting rates in response over the coming weeks. As noted by The Motley Fool, this adjustment provides a timely opportunity for borrowers to secure more favorable loan terms. Lenders are likely to pass on the benefits of the lower federal funds rate to consumers, making personal loans more accessible and affordable.

Examples of pre- and post-cut rate scenarios for unsecured personal loans illustrate the potential savings for borrowers. Before the rate cut, personal loan APRs were higher, reflecting the previous stable-rate environment. Now, with the cut in place, borrowers can expect to see reduced rates, creating a time-sensitive window for refinancing existing debt. This opportunity is particularly beneficial for those looking to consolidate high-interest debt into a single, lower-interest loan.

Variations by lender type, such as how banks versus online platforms respond to the 2025 cut, are also noteworthy. According to CNBC, traditional banks may be slower to adjust their rates compared to more agile online lenders. This difference highlights the importance of shopping around for the best rates and terms, as consumers navigate the changing lending landscape.

Beyond personal loans, the rate cut is likely to influence other consumer credit products. For instance, home equity lines of credit (HELOCs) and adjustable-rate mortgages (ARMs) are directly tied to the federal funds rate. As these rates decrease, homeowners may find it more attractive to tap into their home equity for renovations or other expenses. This could lead to a surge in home improvement projects, benefiting sectors like construction and retail.

Additionally, the rate cut may encourage financial institutions to innovate their product offerings. As competition intensifies, lenders might introduce new loan products or promotional rates to attract borrowers. This environment can be advantageous for consumers who are willing to shop around and compare different lending options, potentially securing better deals than those available in a higher-rate climate.

Opportunities for Borrowers and Savers

With the first rate cut of 2025, there are several smart money moves borrowers can make to capitalize on the new financial environment. As suggested by CNBC, timing new loan applications to secure lower rates is a strategic step. By acting quickly, borrowers can lock in favorable terms before lenders fully adjust their offerings to reflect the new rate environment.

Refinancing strategies for current personal loans are also crucial, emphasizing the urgency as rates begin to decline following the September 2025 announcement. The Motley Fool highlights the benefits of refinancing existing loans to take advantage of lower rates, potentially reducing monthly payments and overall interest costs.

However, potential drawbacks remain, such as unchanged eligibility checks despite the rate cut. As noted by CNBC, borrowers must still meet the same credit and income requirements as before, which can affect their ability to secure new loans. This aspect alters the advice from previous high-rate periods, where eligibility criteria were often a more significant barrier to borrowing.

For savers, the rate cut presents a mixed bag of outcomes. While borrowers benefit from lower interest rates, savers may see reduced returns on savings accounts and certificates of deposit (CDs). As noted by CNBC, this environment encourages savers to explore alternative investment options, such as stocks or bonds, to achieve higher yields. Financial advisors often recommend diversifying portfolios to balance risk and reward, especially in a low-rate environment.

Furthermore, the rate cut could lead to increased consumer spending, as lower borrowing costs free up disposable income. This uptick in spending might stimulate sectors like retail and services, contributing to economic growth. However, consumers should remain cautious about over-leveraging, as future rate adjustments could alter the affordability of debt repayments.

Broader Economic Ripple Effects

The first rate cut of 2025 is expected to influence related borrowing areas, such as credit cards and auto loans, signaling a shift from the tighter conditions of prior years. According to CNBC, these areas may see reduced interest rates, providing additional relief to consumers. This broader impact underscores the interconnectedness of various lending markets and the potential for widespread economic benefits.

Lender responses as of September 24, 2025, include announced rate adjustments for personal loans in direct reaction to the Fed’s action. The Motley Fool reports that some lenders have already begun to lower their rates, reflecting the immediate impact of the rate cut on the lending environment. This responsiveness highlights the dynamic nature of the financial markets and the importance of staying informed about changes.

Forecasts for short-term consumer behavior changes suggest increased loan demand, contrasting with the hesitation seen in earlier 2025 updates. As noted by The Motley Fool, the rate cut may encourage more consumers to take on new loans or refinance existing ones, driving economic activity and potentially boosting consumer confidence. This shift in behavior reflects the broader economic implications of the Federal Reserve’s decision and its potential to stimulate growth.

Silas Redman writes about the structure of modern banking, financial regulations, and the rules that govern money movement. His work examines how institutions, policies, and compliance frameworks affect individuals and businesses alike. At The Daily Overview, Silas aims to help readers better understand the systems operating behind everyday financial decisions.