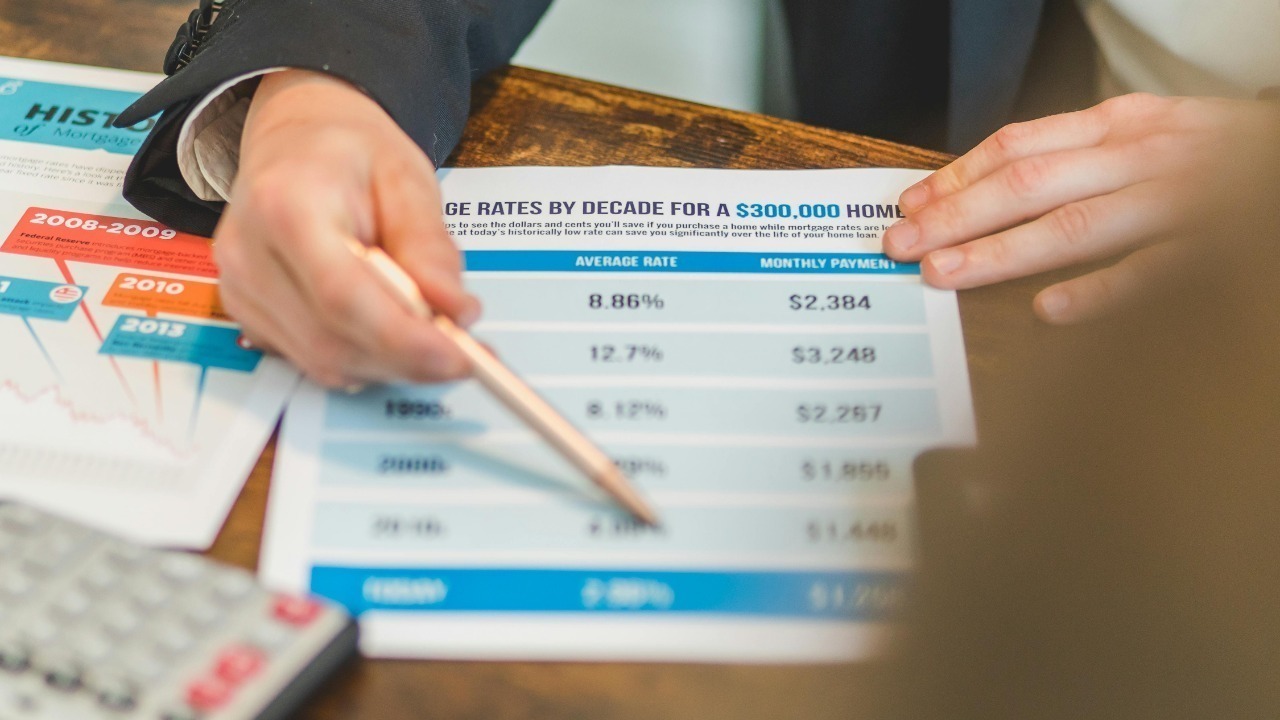

Securing a mortgage pre-approval is a crucial step in the home-buying process. It not only helps you understand how much you can afford but also strengthens your offer when you find the right home. Before you apply, there are several strategic credit moves you can make to improve your chances of getting the best possible terms. Here are 12 essential steps to consider before seeking mortgage pre-approval.

Review Your Credit Report

Start by obtaining a copy of your credit report from the three major credit bureaus: Experian, Equifax, and TransUnion. Reviewing your credit report allows you to understand your current credit standing and identify any areas that need improvement. Look for any discrepancies or outdated information that could negatively impact your score. Regularly checking your credit report is a proactive way to ensure your credit profile is accurate and up-to-date.

Dispute Any Inaccuracies

If you find errors on your credit report, dispute them immediately. Incorrect information, such as a wrongly reported late payment or an account that isn’t yours, can significantly lower your credit score. Contact the credit bureau that provided the report and provide documentation to support your claim. Resolving these inaccuracies can lead to a higher credit score, which is crucial when applying for a mortgage.

Pay Down Credit Card Balances

High credit card balances can negatively affect your credit utilization ratio, which is a key factor in your credit score. Aim to pay down your balances to below 30% of your credit limit. This not only improves your credit score but also demonstrates to lenders that you manage your credit responsibly. Consider using balance transfer cards to consolidate and pay off debt more efficiently. For options, check out the best balance transfer cards of September 2025.

Avoid New Credit Inquiries

Each time you apply for new credit, a hard inquiry is recorded on your credit report, which can temporarily lower your score. Avoid opening new credit accounts or applying for loans in the months leading up to your mortgage application. This helps maintain your current credit score and shows lenders that you are not taking on additional debt.

Keep Old Credit Accounts Open

The length of your credit history is another important factor in your credit score. Closing old accounts can shorten your credit history and reduce your overall available credit, which can negatively impact your score. Keep your oldest accounts open and active to maintain a longer credit history and a higher credit score.

Increase Your Credit Limits

If possible, request a credit limit increase on your existing credit cards. This can improve your credit utilization ratio, provided you don’t increase your spending. A lower utilization ratio can boost your credit score, making you a more attractive candidate for a mortgage. Be sure to use this strategy wisely and avoid accumulating more debt.

Settle Outstanding Debts

Outstanding debts, such as unpaid collections or charge-offs, can significantly impact your credit score. Work on settling these debts before applying for a mortgage. Contact your creditors to negotiate a payment plan or settlement amount. Clearing these debts can improve your credit score and demonstrate financial responsibility to potential lenders.

Establish a Diversified Credit Mix

Lenders prefer to see a mix of credit types, such as credit cards, installment loans, and retail accounts. A diversified credit mix can positively impact your credit score. If your credit profile lacks diversity, consider adding a different type of credit account. However, do this well in advance of your mortgage application to avoid any negative impact from new inquiries.

Maintain Consistent Payment History

Your payment history is one of the most significant factors in your credit score. Ensure all your bills are paid on time, including credit cards, loans, and utilities. Consistent, on-time payments demonstrate reliability and can significantly boost your credit score. Setting up automatic payments or reminders can help you maintain a perfect payment record.

Limit Large Purchases

Large purchases can increase your debt-to-income ratio, which lenders closely examine during the mortgage approval process. Avoid making significant purchases, such as a new car or expensive furniture, before applying for a mortgage. If you already have a car loan, it doesn’t necessarily prevent you from getting a mortgage, but it’s important to manage it wisely. For more insights, read this article on managing car loans and mortgages.

Monitor Your Credit Regularly

Regularly monitoring your credit can help you stay informed about your credit status and detect any unusual activity. Use credit monitoring services or apps to receive alerts about changes to your credit report. Staying on top of your credit can help you address issues promptly and maintain a healthy credit score.

Seek Professional Credit Counseling

If managing your credit feels overwhelming, consider seeking professional credit counseling. A credit counselor can help you create a personalized plan to improve your credit score and financial situation. They can provide valuable advice on budgeting, debt management, and credit repair, helping you become a more attractive candidate for a mortgage.

For more information on whether now is a good time to buy a house, check out this recent article from Yahoo Finance. Additionally, stay informed about the current mortgage rates to better understand the financial landscape as you prepare for your mortgage application.

Elias Broderick specializes in residential and commercial real estate, with a focus on market cycles, property fundamentals, and investment strategy. His writing translates complex housing and development trends into clear insights for both new and experienced investors. At The Daily Overview, Elias explores how real estate fits into long-term wealth planning.