Daily money habits are often small moves that quietly protect your wallet from fraud, surprise bills and slow financial leaks. By treating your wallet, home and shopping choices as part of one security system, you can cut risks without feeling deprived. I focus here on 15 concrete habits, grounded in recent reporting, that you can build into your routine to keep more of your own money.

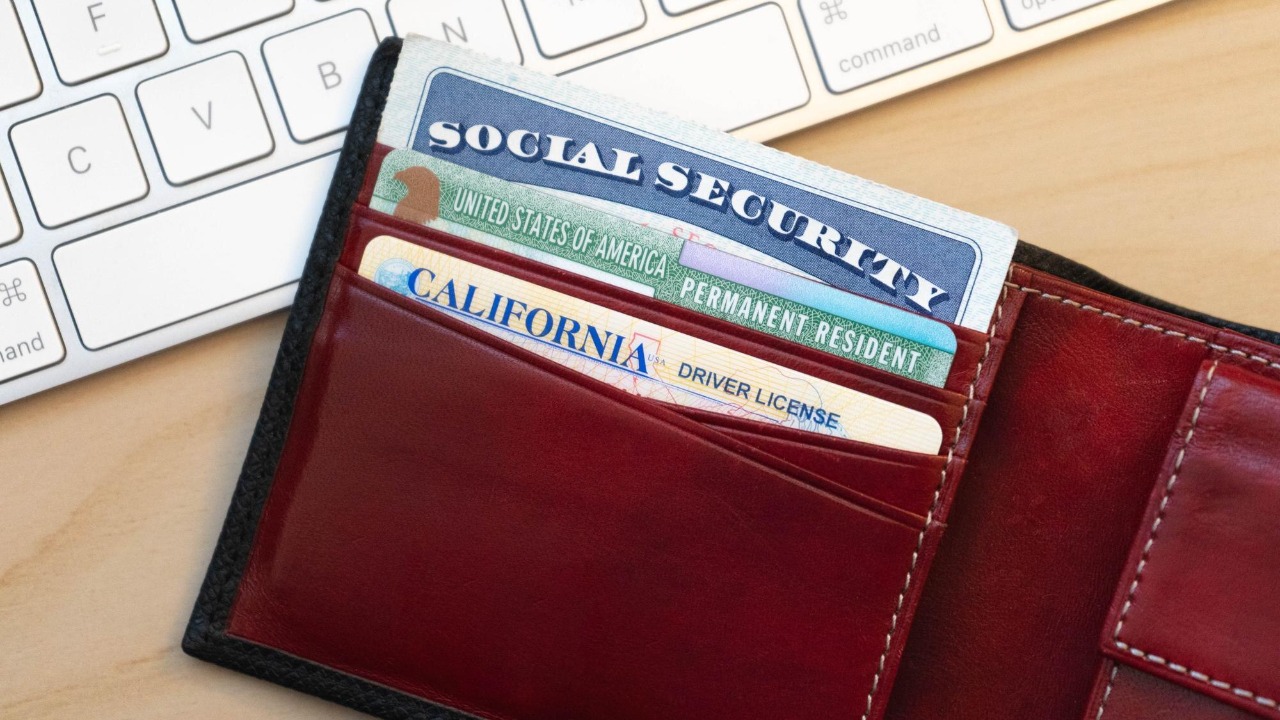

1) Leave your Social Security card at home daily

Leaving your Social Security card at home is one of the most powerful daily habits you can adopt to protect your wallet. Reporting on the worst things to keep in a wallet identifies the Social Security card as a top theft target because it unlocks identity fraud that can drain bank accounts and open bogus credit lines. Other coverage, including lists that warn against Social Security card carry, reinforces that this single document is a gold standard identifier for criminals.

In practice, I treat my Social Security card like a deed or title, not an ID. I memorize the number, store the card in a home safe or safe-deposit box and refuse to carry it for routine errands, doctor visits or job applications. If a business insists on seeing the physical card, I ask why and whether a secure digital upload or masked number will do. The stakes are long term, because once thieves have that number, they can keep abusing it for years.

2) Skip carrying your passport unless traveling

Skipping your passport in everyday life is another simple way to keep your wallet from becoming a jackpot for thieves. The same research on the Worst Things to Carry in Your Wallet highlights that official identity documents are especially dangerous to lose. A passport or passport card does not just confirm your name and birthdate, it also opens the door to international travel risks if someone uses it to cross borders or create forged identities.

I reserve my passport for actual trips, keeping it in a locked drawer or safe the rest of the time. When I travel, I separate it from my everyday wallet, often using a hotel safe or a hidden money belt so a single pickpocket cannot grab everything at once. Losing a passport can trigger emergency replacement fees, canceled flights and extra scrutiny at checkpoints, so treating it as a travel-only document directly protects both your money and your time.

3) Don’t tote your birth certificate in your wallet

Not carrying your birth certificate in your wallet is a daily habit that blocks a key path to identity theft. The reporting on the 15 worst wallet items explains that a birth certificate gives criminals core personal data they can use to forge documents and run financial scams in your name. Other guidance on what cards you should not carry echoes this warning, grouping birth certificates with Social Security cards and passwords as high-risk items.

I only move my birth certificate when I know I will need it for a specific purpose, such as a mortgage closing or a passport application, and even then I carry it in a separate folder rather than my wallet. At home, I store it with other vital records in a fire-resistant box. The broader trend in fraud cases shows that once criminals have both your birth details and other identifiers, they can assemble convincing synthetic identities, so keeping this document out of your daily carry sharply lowers that risk.

4) Keep property deeds in a safe, not your wallet

Keeping property deeds out of your wallet and in a secure location is a habit that protects both your home and your equity. The same wallet-risk reporting notes that carrying a property deed exposes you to real estate fraud, where criminals could attempt to forge signatures, file bogus transfers or use the document to support fraudulent loans. Because a deed proves ownership, losing control of it can trigger expensive legal battles to unwind fraudulent filings.

In my own routine, I treat deeds like irreplaceable legal instruments, storing them in a safe-deposit box or a locked home file rather than anywhere near my everyday wallet. When I need to reference property details, I rely on scanned copies or county records instead of hauling the original around. The financial stakes are enormous, since a forged deed or lien can cloud your title, delay a sale and force you to pay attorneys just to prove you still own what you already paid for.

5) Avoid blank checks in daily carry

Avoiding blank checks in your daily wallet is a direct way to stop thieves from accessing your bank account. The list of worst wallet items points out that blank checks enable direct account drainage if stolen, because they display your routing and account numbers and can be filled out for any amount. Additional guidance on Leave your Checks at home reinforces that criminals can also alter checks payable to you, turning them into quick cash.

I carry a check only when I know I will write it that day, and I never keep a full checkbook in my bag. For recurring payments, I prefer online bill pay or a credit card with fraud protections, which can be shut down quickly if compromised. Treating blank checks like cash, as some experts put it, reframes them as high-value items that do not belong in a crowded wallet where they can be lost, copied or photographed.

6) Store bank account details securely off-person

Storing bank account details somewhere other than your wallet is a daily habit that cuts off another route to unauthorized transfers. The same research on risky wallet contents stresses that exposing routing and account numbers invites criminals to initiate withdrawals, wire transfers or counterfeit checks. Lists of Blank Checks and other sensitive items underline that any document showing full account details is a liability when carried around.

In my day-to-day life, I avoid keeping printed bank statements, deposit slips with full numbers or screenshots of online banking inside my wallet or phone photo roll. Instead, I rely on secure banking apps with biometric logins and avoid writing account numbers on sticky notes or in email drafts. If a thief steals your wallet and finds both your ID and your account details, they have everything they need to impersonate you with customer service and attempt high-dollar transactions.

7) Limit to essential credit cards only

Limiting your wallet to essential credit cards only is a habit that reduces both fraud exposure and potential debt. The wallet-risk reporting flags unused or extra cards as vulnerabilities, because each additional card is another account that can rack up fraudulent charges before you notice. Coverage of 7 things you should never carry in your wallet, where Sullivan warns about Social Security numbers and excess plastic, supports the idea that more cards mean more risk.

I typically carry one primary rewards card and one backup, leaving store cards and infrequently used accounts at home. This makes it easier to monitor transactions in real time with mobile alerts, because I know any unfamiliar charge on those two cards is a red flag. If my wallet is lost, I only have to cancel a couple of accounts instead of a dozen, which shortens the window in which thieves can test stolen numbers online or in stores.

8) Carry minimal cash for daily needs

Carrying only minimal cash for daily needs is a straightforward way to limit the financial damage if your wallet disappears. The analysis of the worst things to keep in a wallet notes that excess cash amplifies loss from pickpockets or theft, because unlike cards, stolen bills cannot be reversed or reimbursed. A separate list of Things You Really Should Not Be Carrying in Your Wallet includes “wads” of cash alongside Social Security cards, Checks, Spare keys and Extra debit cards as avoidable risks.

My own rule is to carry only what I expect to spend that day plus a small buffer, often no more than the amount I would be willing to drop on the sidewalk without panic. For larger purchases, I use a card with fraud protection so I can dispute unauthorized charges if needed. This habit also nudges me to track spending more closely, because I am not relying on a thick roll of bills that can quietly evaporate without leaving a digital trail.

9) Leave spare keys at home or secured

Leaving spare keys out of your wallet is a daily habit that protects both your home and your finances. The reporting on wallet risks warns that Spare keys can lead directly to home break-ins, where thieves may steal electronics, jewelry and important documents that cost thousands to replace. Lists of Things You Really Should Not Be Carrying in Your Wallet also single out Spare keys as a problem because they connect your physical address to your identity documents.

I keep backup house and car keys in a lockbox or with a trusted neighbor instead of in my wallet or glove compartment. If my wallet is stolen with my driver’s license inside, I do not want a thief to have both my address and a working key. The broader trend in burglary cases shows that when criminals can enter without force, insurance claims may be more complicated, and you may face higher deductibles or even coverage disputes.

10) Never write down passwords or PINs in your wallet

Never writing down passwords or PINs in your wallet is a habit that protects every financial account linked to your identity. The same research on dangerous wallet items explains that storing passwords or PINs with your cards directly enables hackers to access all your linked financial services if the wallet is lost. Other guidance on Stowing sensitive data in your wallet stresses that even a partial password list can help criminals guess the rest.

Instead of carrying a paper list, I use a reputable password manager app with strong encryption and a unique master password that I memorize. For card PINs, I avoid obvious patterns like birth years and never write them on the card itself or in a nearby note. If someone steals your wallet and finds both your debit card and its PIN, they can empty your checking account at an ATM long before you have time to cancel the card, turning a simple loss into a full-blown financial emergency.

11) Inspect your home for minor issues each morning

Inspecting your home for minor issues each morning is a habit that keeps hidden maintenance and repair costs from wrecking your budget. Reporting on the hidden costs of homeownership highlights maintenance and repairs as surprise expenses that escalate when ignored. A small leak, for example, can turn into mold remediation or structural damage if it drips unnoticed for weeks, while a loose handrail can become a medical bill if someone falls.

My own routine is quick and simple: I glance at ceilings for water spots, listen for unusual furnace or refrigerator noises and check under sinks for dampness. I also walk the exterior once or twice a week to spot missing shingles or clogged gutters before storms hit. Catching problems early lets me schedule repairs on my terms, compare quotes and avoid emergency call-out fees, which directly protects my wallet from the kind of surprise bills that derail savings plans.

12) Review local tax notices or apps daily for updates

Reviewing local tax notices or property tax apps regularly is a habit that keeps one of homeownership’s biggest ongoing costs from blindsiding your budget. The same analysis of hidden homeowner expenses points to property taxes as recurring charges that can quietly rise and “wreck your budget” if you are not tracking them. Many counties now offer online portals or mobile alerts that flag reassessments, rate changes or new levies that affect your bill.

I make a point of logging into my local tax portal or scanning mailed notices as soon as they arrive, then updating my monthly budget to reflect any change. If I see a sharp increase, I consider whether to appeal the assessment or adjust my escrow contributions so I am not hit with a lump-sum shortage. Staying on top of these numbers helps me avoid late fees, interest charges and surprise escrow adjustments that can push my mortgage payment higher than I planned.

13) Check insurance policy details weekly but confirm coverage daily

Checking your homeowners insurance details weekly and confirming coverage needs daily is a habit that keeps another major hidden cost under control. The reporting on surprise homeowner expenses identifies homeowners insurance as a cost that can spike unexpectedly, especially after claims or regional disasters. Premiums, deductibles and exclusions can all shift over time, leaving you underinsured or overpaying if you are not paying attention.

Once a week, I review my policy declarations page, looking at coverage limits for the dwelling, personal property and liability, and I compare those numbers with current replacement costs. On a daily basis, I think about coverage when I make changes at home, such as buying expensive electronics or starting a home-based business, and I note when I should alert my insurer. This habit helps me avoid painful gaps, like discovering after a storm that my deductible is higher than my emergency fund or that a specific risk was excluded.

14) Switch all home lights to LEDs for daily use

Switching all home lights to LEDs for daily use is a habit that steadily lowers your utility bills while cutting waste. An Earth Day checklist of simple swaps lists LED bulbs as a core change that reduces energy costs over time, because they use far less electricity and last much longer than traditional incandescent bulbs. That means fewer purchases, fewer ladder climbs and a smaller monthly bill.

In my own home, I replace burned-out bulbs with ENERGY STAR rated LEDs and prioritize high-use fixtures like kitchen, hallway and porch lights. I also choose warm color temperatures so the light feels comfortable, which makes it easier to stick with the change. Over a year, the savings from multiple bulbs can add up to meaningful money that stays in your wallet, especially in larger homes or apartments with many always-on lights.

15) Pack a reusable bag before every outing

Packing a reusable bag before every outing is a small habit that protects your wallet from nickel-and-dime fees and impulse purchases. The same Earth Day checklist that highlights LEDs also notes that reusable shopping bags help cut expenses by avoiding plastic bag fees and encouraging more deliberate shopping. Many cities and retailers now charge per disposable bag, so forgetting your own can add a little extra cost to every trip.

I keep compact reusable bags in my car, backpack and coat pockets so I rarely end up paying for single-use bags at checkout. Having a set capacity in those bags also nudges me to stick to my list instead of loading up a cart with unplanned items. Over months, the avoided fees and reduced impulse buys translate into real savings, turning a simple environmental choice into a reliable daily money habit that protects your wallet.

More From TheDailyOverview

- Dave Ramsey warns to stop 401(k) contributions

- 11 night jobs you can do from home (not exciting but steady)

- Small U.S. cities ready to boom next

- 19 things boomers should never sell no matter what

Cole Whitaker focuses on the fundamentals of money management, helping readers make smarter decisions around income, spending, saving, and long-term financial stability. His writing emphasizes clarity, discipline, and practical systems that work in real life. At The Daily Overview, Cole breaks down personal finance topics into straightforward guidance readers can apply immediately.