The Powerball jackpot has surged to $1.5 billion, a headline number that instantly triggers daydreams about private jets, early retirement, and never checking a price tag again. The reality is more complicated, because the winner will face a series of choices and tax hits that dramatically shrink that figure before a single dollar is spent. To understand what the lucky ticket holder could actually keep, I walked through the cash option, federal rules, and how state taxes and smart planning can change the final take-home.

How a $1.5 billion jackpot really breaks down

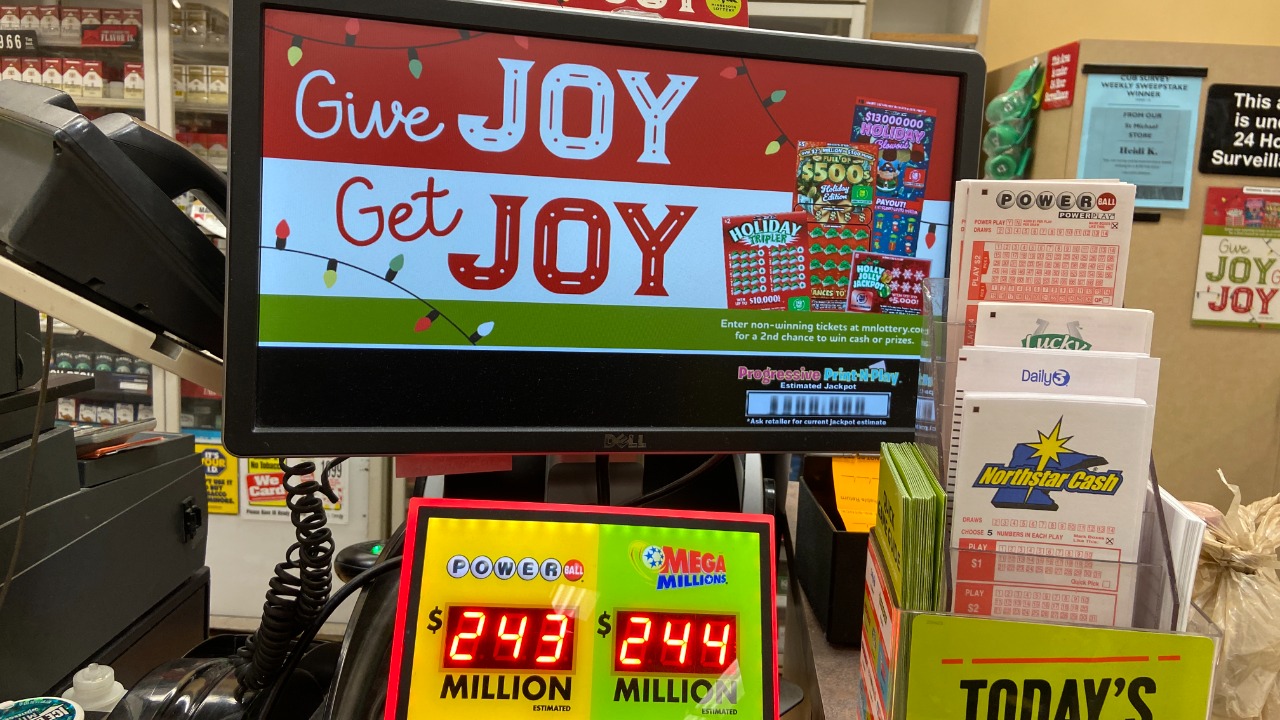

When Powerball climbs into ten-figure territory, the advertised jackpot reflects an annuity paid out over three decades, not a lump sum wired to your bank account. For a $1.5 billion prize, recent estimates suggest a single winner could instead choose a cash payout of $686.5 million, a figure that already shows how much of the headline total is tied up in long term interest assumptions. That cash option is the starting point for every other calculation, because taxes are applied to the amount you actually receive, not the billboard number.

The current drawing has become one of the largest in Powerball history after a long stretch without a grand prize winner, with officials noting that Saturday’s jackpot would rank among the game’s five biggest and that it marks only the second time Powerba has crossed this threshold. As Powerball is rolling into this drawing, the pot has been fueled by a record losing streak and a surge of last minute ticket buyers. Each $2 play not only feeds the jackpot but also helps fund public programs in participating states, so the eye popping total reflects both player demand and the way the game is structured to grow quickly when no one hits all six numbers.

Federal taxes: the first and biggest bite

The federal government treats lottery winnings as ordinary income, which means a jackpot winner is pushed straight into the top tax bracket. On a prize of this size, Federal rules trigger automatic withholding as soon as the ticket is cashed, and the Internal Revenue Service expects its cut whether you choose the annuity or the lump sum. For a recent $1.7 billion prize, reporting noted that Federal taxes would immediately claim up to 37%, a rate that also applies to a $1.5 billion jackpot winner once total income is tallied.

On top of that top bracket, there is a separate rule for withholding on gambling windfalls. Federal tax withholdings immediately claim 24% of winnings exceeding $5,000, which means nearly a quarter of that $686.5 million cash option is siphoned off before the winner ever sees it. On a previous $1.8 billion jackpot, that 24% withholding left about $628 million in the winner’s hands at first, but the final bill was higher because the top bracket required another round of federal taxes, an additional $107 million. The same pattern would apply here, with the initial withholding followed by a year end reckoning that pushes the effective rate closer to that 37% ceiling.

State taxes and where you buy your ticket

After the federal government takes its share, the next question is where the winning ticket was sold and where the winner lives. Some states treat lottery jackpots as taxable income, while others do not tax them at all, and that difference can mean millions of dollars over time. In earlier coverage of a $1.7 billion drawing, analysts pointed out that some states add their own income tax on top of the federal bill, while others such as Florida and California do not tax lottery prizes, a contrast highlighted when explaining how Federal taxes would immediately claim up to 37% but state rules vary widely.

All Powerball wins are subject to state and federal taxes in the sense that every jurisdiction has its own rules, and the game itself reminds players that they need to check local law. The official ticketing platforms note that All Powerball prizes are reported and that winners may owe additional amounts depending on where they live and where they bought the ticket. That means a winner in New York or New Jersey could see a significant extra bite compared with someone in Texas or Washington, even if both chose the same cash option and had identical federal obligations.

Annuity versus lump sum: what the choice really means

Every Powerball jackpot winner faces a pivotal decision between taking the annuity or the lump sum, and the choice shapes both taxes and long term security. The annuity spreads payments over 30 years, which keeps each year’s taxable income lower and can reduce the impact of the top federal bracket, while the lump sum front loads the income into a single tax year. In practical terms, the annuity is what turns a $1.5 billion headline into a series of gradually increasing checks, while the lump sum compresses that value into the roughly $686.5 m cash payout that is then taxed all at once.

Financial planners often argue that the right choice depends on the winner’s discipline and support system, not just the math. Earlier breakdowns of nine and ten figure jackpots have shown that even after taxes, a lump sum can leave hundreds of millions of dollars to invest, but the annuity can act as a guardrail against overspending and bad investments. In one recent analysis of a $1.25 billion prize, experts walked through how the advertised total shrinks after taxes and how the structure of the annuity compares with the cash option, using the Dec drawing to illustrate how much a winner would actually keep after choosing between the two paths and paying the required taxes on the Dec jackpot.

How the jackpot got this big and where the money goes

The sheer size of the current prize is not an accident, it is the product of game design that lets jackpots snowball when no one hits all six numbers. Saturday marks the 45th Powerball drawing in the current run without a grand prize winner, a streak that has allowed the pot to swell to $1.5 billion. As one lottery official explained, the jackpot grows with every $2 ticket sold, and a portion of each ticket supports local public programs and services, a point emphasized when noting that the jackpot grows with every $2 ticket and that this drawing ranks among the fifth largest in the game’s record books.

That growth has been closely watched by lottery officials such as Chris Benson, who has been tracking how each rollover adds to the total and how public interest spikes as the pot climbs. In coverage of the current run, Chris Benson described how Saturday’s drawing has become a national event, with ticket sales surging across multiple states and the Iowa Lottery’s CEO highlighting the unprecedented length of the streak. That surge does not just feed the jackpot, it also boosts the funds that state lotteries send to education, infrastructure, and other earmarked programs, which is why officials lean into the public benefit message when the numbers get this large.

What a winner could actually keep after all the cuts

Once the mechanics are clear, the natural question is how much money a winner would realistically have to spend or invest after the dust settles. Starting from the roughly $686.5 million cash option, the initial 24% federal withholding would carve out more than $160 million immediately, leaving something in the neighborhood of the $628 million seen in the earlier $1.8 billion example, where the first round of withholding left $628 m before the final bill. After the year end tax return pushes the effective rate toward that 37% top bracket, the federal share alone could approach or exceed a quarter of a billion dollars, and state taxes could add tens of millions more depending on the jurisdiction.

Even after those cuts, the remaining sum is still life changing, but it is far from the $1.5 billion that dominates the headlines and the daydreams. Earlier explainers on a $1 billion jackpot walked through how the federal government counts lottery winnings as income and how, because the prize is so large, winners can owe another 13% of that prize beyond the initial withholding, a pattern that would scale up for a $1.5 billion pot as Because the federal government counts every dollar as taxable income. That is why financial advisers urge winners to assemble a team of professionals before claiming the ticket, to think carefully about whether to share the prize with family members, and to remember that even a reduced nine figure windfall can disappear quickly without a plan.

For everyone else, the lesson is that the Powerball dream is as much about understanding the fine print as it is about picking the right numbers. The game itself reminds players that detailed rules, odds, and tax information can be found on official channels, and recent coverage of an $875 million run pointed people to the official Powerball website for more details on how the drawings work and how prizes are paid, noting that For those interested in more details, the official site is the best source. The odds of winning remain microscopic, but if lightning does strike, the difference between the headline number and the amount you actually keep will come down to tax law, geography, and the choices you make in the first frantic days after the drawing.

More From TheDailyOverview

Julian Harrow specializes in taxation, IRS rules, and compliance strategy. His work helps readers navigate complex tax codes, deadlines, and reporting requirements while identifying opportunities for efficiency and risk reduction. At The Daily Overview, Julian breaks down tax-related topics with precision and clarity, making a traditionally dense subject easier to understand.