Student loan debt has become a defining feature of modern education. While many wealthy individuals may have bypassed these challenges, the realities faced by those in debt are profound and multifaceted. Understanding the complex nature of student loans can bridge the empathy gap, providing insight into the financial and emotional toll they impose.

The Weight of Accumulating Interest

Interest on student loans starts to build up long before graduation day arrives. This accumulating interest can turn a manageable loan balance into a seemingly insurmountable financial burden over time. For many, it feels like running on a treadmill, never quite catching up with the loan amount they initially borrowed.

Many borrowers find themselves paying off interest rather than the principal, leading to a cycle of debt that extends far beyond their college years. This situation is exacerbated by the fact that some types of loans, such as unsubsidized federal loans, accrue interest while the borrower is still in school.

The Impact on Career Choices

Student loans often influence career decisions, with many graduates opting for higher-paying jobs rather than pursuing their passions. This pragmatic approach is driven by the need to manage monthly loan payments, leaving little room for risk-taking or career exploration.

Fields such as education, arts, and non-profits often suffer because potential candidates view them as financially unsustainable. For instance, a graduate with a degree in social work may feel compelled to choose a corporate path instead of helping communities, due to the promise of a higher salary.

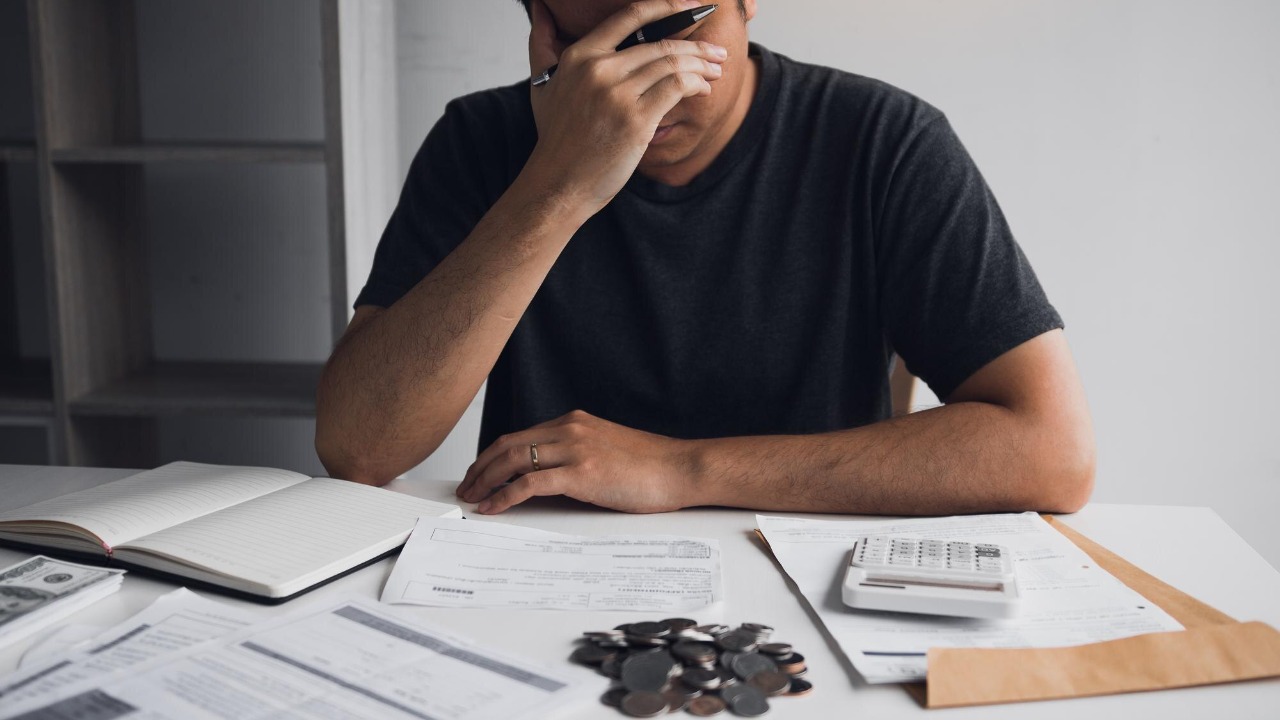

The Strain on Mental Health

The stress associated with student loan debt can significantly impact mental health. Anxiety, depression, and feelings of hopelessness are common among borrowers who feel trapped by their financial obligations.

According to research, the psychological impact of debt affects not only personal well-being but also relationships and job performance. The constant pressure to meet payment deadlines can lead to burnout and a reduced quality of life.

The Delay in Major Life Milestones

Student loan debt often delays significant life events such as marriage, homeownership, and starting a family. The financial uncertainty that comes with monthly loan payments makes it difficult for many to commit to these milestones.

For example, a 2024 New York Times article highlights how millennials are postponing buying homes due to debt, which affects the housing market and economic growth. This delay creates a ripple effect, impacting not just individuals but society as a whole.

The Disparity in Loan Terms

Loan terms can vary widely, creating disparities in how debt is managed and repaid. Federal loans often have more favorable terms than private loans, but not everyone qualifies for them.

These disparities can lead to unequal financial stress among borrowers, exacerbating existing inequalities in education. This situation often leaves those with private loans struggling with higher interest rates and less flexible repayment options.

The Burden of Repayment Plans

While repayment plans are designed to ease the financial burden, they can sometimes add to the complexity and stress of managing student loans. Graduates often find themselves navigating a maze of options, each with its own set of rules and implications.

Income-driven repayment plans can extend the repayment period, increasing the total interest paid over time. Borrowers must weigh the pros and cons, often without adequate financial guidance, which can lead to costly mistakes.

The Challenge of Loan Forgiveness Programs

Loan forgiveness programs promise relief but are often fraught with challenges and barriers. Many borrowers do not fully understand the eligibility criteria, which can change based on legislation and policy shifts.

Programs like Public Service Loan Forgiveness require a decade of qualifying payments and employment, creating uncertainty about their effectiveness. As a result, many borrowers are left disappointed, as highlighted by Ramsey Solutions.

The Struggle for Financial Independence

Student loans can hinder financial independence long after graduation. The obligation to repay loans can prevent individuals from building savings, investing, or pursuing entrepreneurial ventures.

For many, achieving financial independence feels like an elusive goal, as they juggle loan repayments with other living expenses. This struggle is especially evident among millennials, who face a unique set of economic challenges.

The Inequality in Access to Education

Student loans highlight the inequality in access to higher education. Wealthier families can often pay tuition out-of-pocket, while others rely on loans to access the same opportunities.

This inequality perpetuates a cycle where only those with financial means can comfortably afford a college education, as discussed in various studies. This disparity affects not only individuals but society as a whole, as it limits diversity in higher education.

The Pressure of Default Consequences

The consequences of defaulting on student loans are severe and long-lasting. Borrowers face damaged credit scores, wage garnishment, and even legal action, which can compound their financial troubles.

Defaulting also limits access to future loans and housing opportunities, making it difficult to recover financially. The fear of these consequences adds another layer of stress for borrowers who are struggling to make ends meet.

The Complexities of Refinancing Options

Refinancing student loans can offer lower interest rates and simplified payments, but it comes with its own set of complexities. Borrowers must navigate the fine print, often without expert guidance.

Refinancing federal loans into private ones can result in the loss of benefits like income-driven repayment plans and forgiveness programs. Therefore, understanding the trade-offs is crucial for making informed financial decisions.

The Long-Term Financial Constraints

Student loan debt can have long-term financial constraints that extend well into retirement. Borrowers may find themselves still paying off loans as their own children enter college.

This extended financial pressure can limit retirement savings and financial security in later life, creating a cycle of debt across generations. Understanding these long-term implications is essential for both borrowers and policymakers.

Silas Redman writes about the structure of modern banking, financial regulations, and the rules that govern money movement. His work examines how institutions, policies, and compliance frameworks affect individuals and businesses alike. At The Daily Overview, Silas aims to help readers better understand the systems operating behind everyday financial decisions.