Many baby boomers in America are facing serious financial challenges as they approach retirement or are already in it. A combination of factors, including economic shifts, inadequate savings, and unexpected expenses, have put many in precarious positions. The following sections explore the critical reasons behind their financial struggles and examine whether any of these issues might apply to you.

Inadequate Retirement Savings

One of the most pressing issues is the lack of adequate retirement savings. Many baby boomers did not prioritize saving for retirement early in their careers. During the 1960s and 1970s, when many boomers were entering the workforce, the emphasis was less on individual retirement savings plans and more on employer-provided pensions, which have since become far less common. Without structured superannuation plans, many boomers found themselves unprepared for retirement when the time came. According to financial experts, this lack of early planning is a significant contributor to their current financial woes.

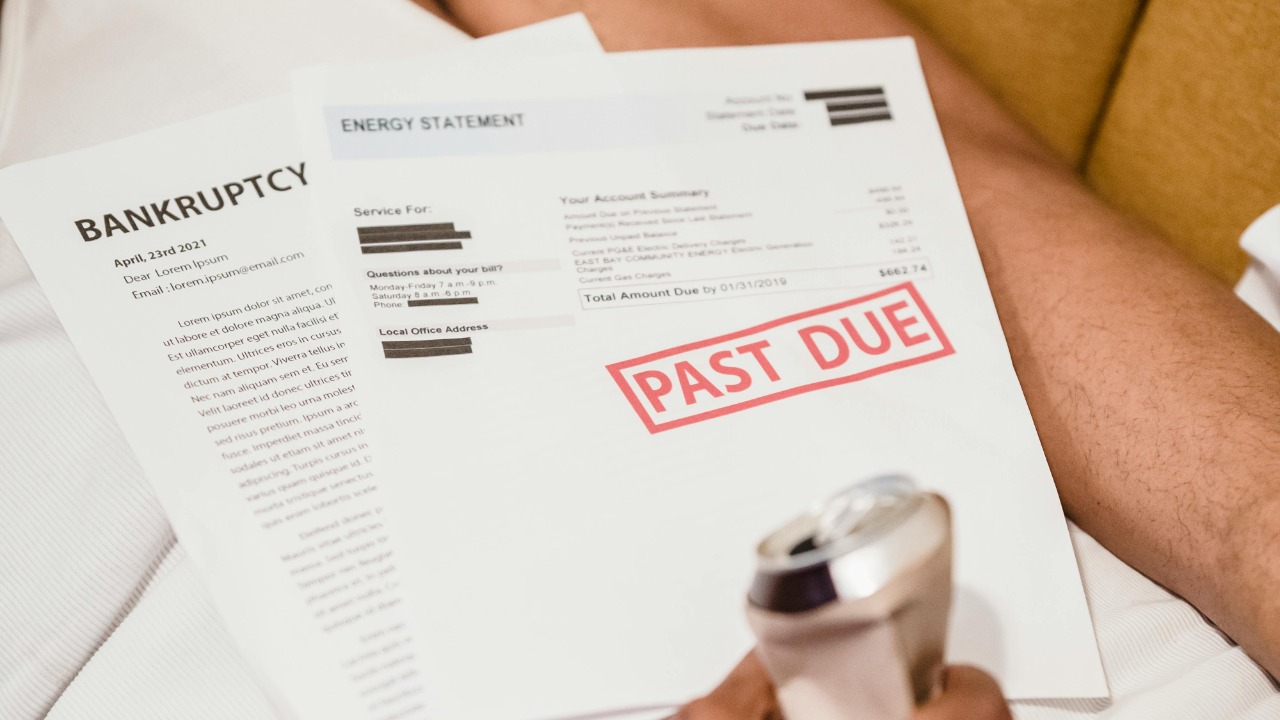

Compounding the issue is the rising cost of living. Inflation has eroded the purchasing power of savings, making it challenging for retirees to maintain their desired lifestyle. For instance, the cost of basic necessities such as housing, food, and healthcare has escalated over the decades. This has forced many to dip deeper into their savings than initially planned. Additionally, the reliance on Social Security benefits has proven insufficient for many. Social Security was designed to supplement retirement savings, but for many boomers, it has become the primary source of income, leaving them financially vulnerable when it falls short.

Healthcare and Medical Expenses

Healthcare costs have skyrocketed over the years, placing an immense financial burden on baby boomers. This increase is not just in premiums but also in out-of-pocket expenses for treatments and medications. Many boomers did not anticipate the high cost of healthcare in their retirement planning, leading to financial strain. As they age, the likelihood of requiring long-term care increases, further compounding the financial challenges. The rising costs often exceed expectations, leaving many struggling to afford necessary care.

Additionally, inadequate health insurance coverage has left many boomers facing significant out-of-pocket expenses. While Medicare provides a safety net, it does not cover all medical expenses, leaving gaps that must be filled by other means. This is particularly challenging for those with chronic health issues, which are prevalent in the boomer generation. Conditions such as diabetes, heart disease, and arthritis require ongoing management and medication, leading to continuous financial outlays that quickly deplete savings.

Debt and Financial Obligations

Debt is a major concern for many baby boomers. Unlike previous generations, many boomers enter retirement with substantial debt, including mortgages, credit cards, and personal loans. Economic downturns have exacerbated this issue, leading to increased borrowing and, consequently, higher debt levels. The 2008 financial crisis, in particular, had a profound impact, resulting in job losses and decreased investment returns. According to financial analyses, this has left many boomers struggling to manage their financial obligations.

Adding to the challenge is the financial support many boomers provide for family members, including adult children and aging parents. This support can significantly interfere with their ability to save for retirement or pay down debt. The need to assist family members financially often arises unexpectedly, leading to further financial strain. This situation is exacerbated by broader economic factors, such as rising housing costs, which make it difficult for younger generations to become financially independent.

Workforce Challenges and Retirement Planning

The job market presents unique challenges for older workers. Age discrimination, whether implicit or explicit, limits job opportunities for boomers seeking to supplement their retirement income. Many find themselves unable to secure employment that matches their skill level or experience. This lack of opportunity forces some to accept lower-paying jobs or remain unemployed, making it difficult to improve their financial situation. Additionally, the need to delay retirement due to financial necessity can lead to a decreased quality of life and disrupt long-term plans.

Another critical issue is the lack of financial literacy among some baby boomers. Without a solid understanding of financial planning and investment strategies, many have been ill-prepared to make informed decisions regarding their retirement. This gap in financial education often results in poor investment choices, insufficient savings, and a lack of understanding of how to maximize retirement benefits. Increased access to financial education could help address these challenges, enabling boomers to make more informed decisions about their financial futures.

Economic and Policy Factors

Changes in pension systems have significantly impacted baby boomers. The shift from defined benefit plans, which guaranteed a specific payout upon retirement, to defined contribution plans has placed financial risk on the employees. This transition means that individuals are now responsible for managing their own retirement savings and ensuring they have enough to last through their retirement years. Unfortunately, not everyone has the knowledge or skills to manage these funds effectively, leading to shortfalls.

Policy changes have also played a role in the financial challenges faced by boomers. Modifications to social security and pension policies have reduced expected benefits, directly affecting their financial stability. For example, adjustments to the age of eligibility for full social security benefits mean that many have to wait longer to receive their full entitlements. Additionally, broader economic trends, such as income inequality and wealth distribution, have exacerbated these issues, disproportionately affecting the financial security of many boomers. Addressing these systemic issues will require coordinated efforts at both policy and community levels.

Cole Whitaker focuses on the fundamentals of money management, helping readers make smarter decisions around income, spending, saving, and long-term financial stability. His writing emphasizes clarity, discipline, and practical systems that work in real life. At The Daily Overview, Cole breaks down personal finance topics into straightforward guidance readers can apply immediately.