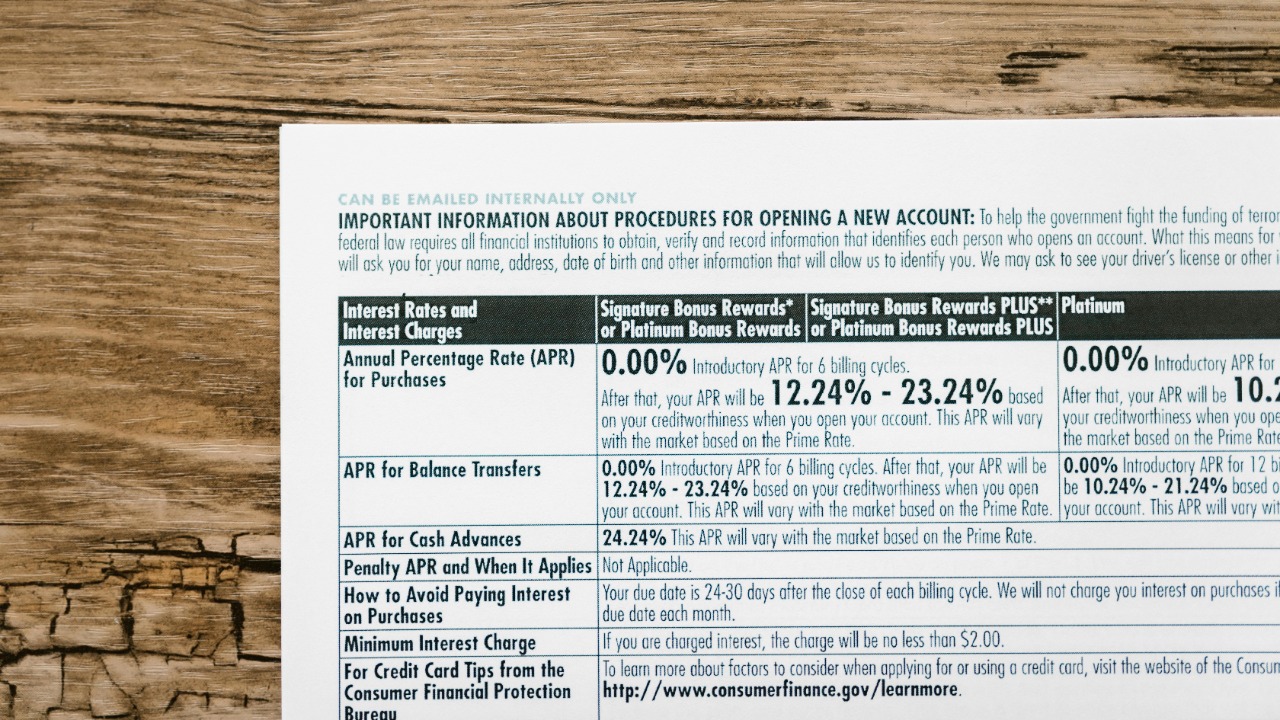

In 2023, the average credit card balance in the United States reached $6,501, underscoring the widespread challenge of managing revolving debt amid rising interest rates that can exceed 20% APR on many cards. A persistent myth suggests that carrying a small balance month-to-month can boost your credit score by demonstrating active use. However, this overlooks how unpaid interest accrues and inflates credit utilization ratios, potentially lowering scores instead. Effective credit building focuses on paying balances in full each month to maintain low utilization under 30%, which comprises about one-third of FICO scoring models, rather than risking debt accumulation.

How Credit Scores Are Calculated

The FICO model, which is widely used to calculate credit scores, considers several key factors. Payment history accounts for 35% of the score, while amounts owed make up 30%, and the length of credit history contributes 15%. Within the amounts owed category, credit utilization measures balances against limits rather than rewarding ongoing balances. This means that carrying any balance, even a small one, can signal risk to lenders if it leads to interest charges. In contrast, maintaining zero balances can optimize scoring algorithms by demonstrating responsible credit management according to NerdWallet.

Carrying a balance can have unintended consequences on your credit score. For example, scores can drop when utilization exceeds 30% due to perceived over-reliance on credit. This is because high utilization ratios suggest to lenders that you may be overextended financially, which can negatively impact your creditworthiness, as reported by CBS News.

The Myth of Carrying a Small Balance

The outdated idea that making minimum payments on a small balance demonstrates “creditworthiness” to credit bureaus stems from pre-2000s scoring misunderstandings. Today, this practice invites unnecessary interest costs averaging 21% APR without providing any score gains. For instance, carrying a $100 balance at 20% APR adds $20 yearly in fees, whereas paying in full keeps utilization at 0% for positive reporting, as explained by Bankrate.

Average U.S. debt levels, such as the $6,501 figure, illustrate how small balances can snowball, harming long-term financial health more than helping credit scores. This highlights the importance of dispelling myths that encourage carrying balances, which can lead to accumulating debt rather than building credit effectively, according to Forbes.

Impact of Credit Utilization on Your Score

Credit utilization is calculated as the ratio of current balances to total credit limits. To boost your credit score, it’s advisable to keep this ratio below 30%—ideally 10% or less—regardless of whether a balance is carried. This approach ensures that your credit report reflects responsible credit use without the risk of accruing interest charges.

Revolving balances reported to credit bureaus reflect snapshot data from statement closing dates. This means that even small unpaid amounts can temporarily spike utilization and cause scores to dip. For high-debt groups, such as seniors facing average debts of $6,501, carried balances exacerbate APR burdens without offering utilization benefits.

Strategies to Build Credit Without Carrying Balances

Paying balances in full each month to report 0% utilization, combined with on-time payments, is the safest path to improving your credit score without falling into interest traps. Alternatives like balance transfer cards with 0% introductory APR periods can help consolidate small debts interest-free, avoiding the pitfalls of carrying balances while managing utilization effectively.

For vulnerable groups, such as seniors, using debt management plans or credit counseling can help eliminate balances entirely, reducing average loads like the $6,501 national figure. These strategies not only improve credit scores but also enhance overall financial health by preventing debt accumulation.

Long-Term Effects of Balance-Carrying Habits

Habitually carrying small balances can lead to compounding interest at rates over 20% APR, potentially turning minor debts into larger ones that weigh down credit utilization and scores over time. This practice contrasts with debt-free habits that build positive credit history, warning against myths that could contribute to the $1.13 trillion total U.S. credit card debt burden.

Monitoring your credit through free annual credit reports can help track utilization impacts, emphasizing the importance of full payoff as key to sustained score health. By understanding and applying these principles, individuals can avoid the pitfalls of carrying balances and instead focus on strategies that genuinely enhance their credit profiles.

Cole Whitaker focuses on the fundamentals of money management, helping readers make smarter decisions around income, spending, saving, and long-term financial stability. His writing emphasizes clarity, discipline, and practical systems that work in real life. At The Daily Overview, Cole breaks down personal finance topics into straightforward guidance readers can apply immediately.